Direct Business Lenders vs. Brokers: Choosing the Right Funding Path in 2026

- anthonyarallen

- 11 minutes ago

- 12 min read

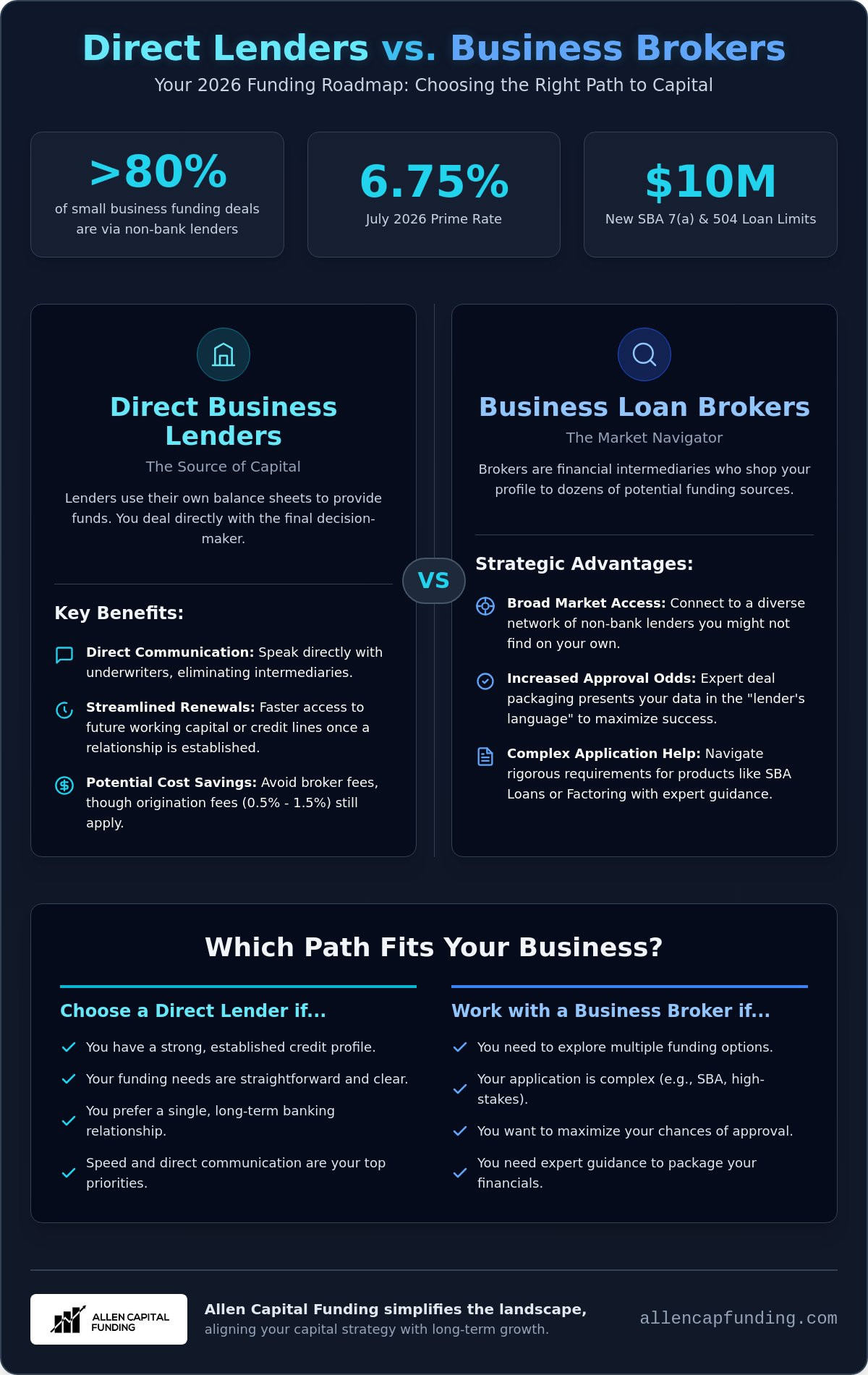

Over 80% of small business funding deals in 2026 now occur through non-bank funders. If you've faced rejection from traditional banks or feel overwhelmed by complex fee structures, your frustration is understandable. Choosing between direct business lenders vs brokers is a strategic decision that impacts your speed of growth and your bottom line. With the July 2026 Prime Rate at 6.75%, selecting the wrong path can lead to unnecessary costs and missed opportunities. Many owners worry about who actually controls the capital and whether they're paying for a service they could find themselves.

You need a reliable guide to help you secure the most cost-effective capital without the typical confusion. This guide clarifies the differences between direct lenders and brokers so you can achieve higher approval probabilities and lower interest rates. We will examine the current lending landscape, including the updated $10 million SBA loan limits and the impact of new state-level disclosure laws on transparency. By the end, you'll have a clear roadmap to the funding that best supports your business's accelerated success and long-term stability.

Table of Contents

Understanding the Fundamental Divide: Direct Lenders vs. Brokers

The 2026 capital market has shifted. While traditional banks remain a fixture, non-bank funders now handle approximately 80% of small business funding deals. This massive migration means the choice between direct business lenders vs brokers is no longer just about comparing interest rates. It's about how you access the market and who holds the power over your approval. A direct lender provides the funds and manages the debt internally. A broker manages the search, the paperwork, and the application strategy to find the best fit. Understanding this divide ensures you don't waste time on paths that lead to rejection or high fees.

The core distinction is simple. A lender manages the debt; a broker manages the search. When you apply to a direct lender, you're asking one entity for their specific money. When you work with a broker, you're hiring an expert to shop your profile to dozens of potential sources. With the July 2026 Prime Rate sitting at 6.75%, the efficiency of your application process directly impacts your final cost of capital.

What is a Direct Business Lender?

Direct lenders are institutions that use their own balance sheets to provide capital. This group includes commercial banks, credit unions, and independent debt funds. When you work with them, you're dealing with the final decision-maker. They set the underwriting criteria, approve the credit, and wire the funds directly to your business account. This path is often ideal for established firms with high credit scores who want to build a singular, long-term relationship.

Direct Communication: You speak with the underwriters who actually sign off on your loan.

Potential Cost Savings: You may avoid intermediary fees, though you'll still face origination costs.

Streamlined Renewals: Once you're in their system, securing additional Working Capital or Credit Lines is often faster.

What is a Business Loan Broker?

A business loan broker acts as a Financial Intermediary between your company and multiple lending sources. They don't lend their own money. Instead, they package your financial data to meet the specific "boxes" of various lenders. This is essential for complex products like SBA Loans or Factoring, where the application requirements are rigorous. Brokers are valuable because they know which lenders have an appetite for your specific industry or credit profile at any given moment.

In 2026, as the SBA has doubled loan limits for 7(a) and 504 programs to $10 million, brokers help navigate these higher-stakes applications. They ensure every document is perfectly aligned with current federal requirements before the lender even sees it. This expertise often makes the difference between an outright rejection and a successful funding round. When weighing direct business lenders vs brokers, remember that the broker's goal is to maximize your approval odds by presenting your data in the "lender's language."

The Case for Direct Business Lenders: Speed and Direct Relationships

Working directly with a source of capital offers a level of transparency that many business owners prefer. When you evaluate direct business lenders vs brokers, the primary appeal of the direct route is the absence of a middleman. You deal with the institution that actually holds the capital. This creates a clear line of communication between your business and the person signing the check. You aren't playing a game of telephone; you're speaking with the underwriters who understand the nuances of your balance sheet.

Long-term partnerships are the bedrock of direct lending. Most commercial banks and debt funds reward loyalty through what's known as a depository relationship. In 2026, maintaining your primary operating accounts with your lender often acts as a hedge against volatility, potentially securing more favorable terms on Credit Lines or Equipment Financing. Once you've established this trust, subsequent funding rounds or renewals are often fast-tracked because the lender already has your historical data on file.

Cost efficiency remains a major driver for this path. Traditional banks typically charge origination fees between 0.5% and 1.5%. By skipping a broker, you avoid potential referral fees that might be baked into the loan's total cost. This makes direct lending a highly cost-effective path for companies that already fit a standard "lender box" and have the internal resources to manage the application process themselves.

When Direct Lending Wins

Standard "vanilla" deals are the perfect fit for direct lenders. If your business boasts a high credit score, consistent revenue, and clear collateral, a direct application is often the fastest route. For those seeking government-backed options, the SBA Lender Match program provides a helpful starting point to find participating direct institutions. In 2026, the depository advantage is clear: businesses that keep their cash reserves with their lending bank can often negotiate lower interest rate margins than those using external funders.

Potential Drawbacks of Going Direct

The main risk of going direct is the "all or nothing" nature of the application. If a bank denies your request, you've spent weeks on a single dead end. Traditional business loan approval rates currently hover between 15% and 35% for quality applications. This rigid criteria means a small dip in credit or a specific industry classification can trigger an automatic "hard stop." You also bear the full burden of document preparation and market shopping. To avoid these pitfalls, consider a strategic financial check-up to ensure your profile is ready before you approach a direct institution.

The Strategic Advantage of Business Loan Brokers: Market Access and Expertise

While direct lenders offer a straight line to capital, brokers provide a wide-angle lens on the entire market. In 2026, the sheer variety of non-bank capital sources can be overwhelming for a busy owner. Brokers serve as a bridge to private debt funds, asset-based lenders, and specialized fintech firms that don't market directly to the public. Understanding how business loan brokers work is essential for any business that doesn't fit the rigid "vanilla" profile of a traditional commercial bank. They don't just find money; they translate your complex financial history into a narrative that matches specific underwriting algorithms.

The debate between direct business lenders vs brokers often centers on cost, but this ignores the power of competitive bidding. A skilled broker forces multiple lenders to compete for your business. This competition frequently results in lower interest rates or more flexible repayment terms that effectively offset any broker-related fees. Beyond the numbers, brokers provide the strategic foresight to identify signs you need working capital before a cash crunch becomes a crisis. They ensure you're applying for the right amount at the right time.

Navigating Complex Funding Products

Certain financial vehicles are too intricate for a "DIY" application. SBA loans, for instance, involve layers of federal compliance that can delay funding for months if handled incorrectly. With the 2026 increase in SBA 7(a) limits to $10 million, the stakes are higher than ever. Brokers also facilitate niche solutions like purchase order financing for inventory, which requires precise coordination between suppliers and funders. Whether it's specialized equipment financing or complex factoring, a broker ensures your deal is packaged to meet the specific requirements of the most aggressive lenders in that space.

Brokers as Long-Term Financial Allies

A broker's value extends far beyond a single transaction. They act as a buffer for your credit score, utilizing soft-pull pre-qualifications that have become the industry standard in 2026. This allows you to shop for terms without the damage of multiple hard inquiries. They also shoulder the heavy paperwork burden, managing the back-and-forth with underwriters so you can focus on daily operations. By conducting regular financial check-ups, a broker helps you build a capital strategy that evolves as your business grows, acting as a proactive ally rather than a distant financial entity.

Decision Framework: Which Path Fits Your Current Capital Needs?

Choosing the right path between direct business lenders vs brokers requires a clear-eyed look at your balance sheet and your timeline. It isn't a permanent choice, but it is a critical one for your immediate growth. While we've explored the individual strengths of each model, your current capital needs should dictate your first move. High FICO scores and stable tax returns usually point toward direct lenders. If your credit is challenged or your revenue fluctuates, brokers provide the necessary market reach to find flexible underwriters who look beyond a single score.

Funding urgency also plays a major role. Direct lenders are often faster for simple renewals because they already have your historical data. However, brokers are typically faster for first-time alternative funding. They know which lenders are aggressively deploying capital in 2026 and which have tightened their belts. If your business operates in a high-risk sector like construction, trucking, or cannabis, a broker's ability to shop multiple non-bank funders becomes your greatest strategic advantage. They prevent you from wasting weeks on applications that are destined for an automatic "industry risk" rejection.

The complexity of your "capital stack" is the final factor. Do you need a single, straightforward term loan? Or does your strategy require a mix of a line of credit for emergencies and factoring for unpaid invoices? Brokers excel at building these multi-layered solutions. They manage the inter-creditor agreements that direct lenders often find cumbersome. Use the checklists below to determine where you should focus your energy today.

The "Direct First" Checklist

Credit Profile: You have a 720+ FICO score and can provide at least two years of profitable tax returns.

Funding Type: You are seeking a simple term loan or a business line of credit for standard operations.

Existing Infrastructure: You already have a dedicated commercial loan officer at your bank who understands your business model.

Complexity: You only need a single capital product without complex collateral requirements.

The "Broker First" Checklist

Recent History: You have been turned down by your primary bank or a direct lender in the last 90 days.

Specialized Needs: You need specialized asset-based lending for small business to unlock balance sheet liquidity.

Leverage Goals: You want to secure the maximum possible leverage by utilizing multiple funding products simultaneously.

Market Access: You want to force lenders to compete for your business to ensure you're getting the best possible terms in the current 6.75% Prime Rate environment.

If you're unsure which checklist fits your current situation, you don't have to guess. You can schedule a strategic financial check-up to analyze your profile and identify the most efficient path to capital for your business.

How Allen Capital Funding Simplifies the Funding Landscape

Allen Capital Funding operates as your dedicated guide in a complex financial world. We recognize that the choice between direct business lenders vs brokers is often a false dilemma for the modern entrepreneur. You don't need a middleman who simply passes paperwork; you need a strategic partner who understands the 2026 capital markets. Our hybrid philosophy combines the authoritative expertise of a financial consultant with the broad market access of a top-tier broker. We represent your interests across all 50 states, ensuring you secure the capital necessary for accelerated success.

We focus on clarity and efficiency. In an environment where over half of bank applicants face rejection or underfunding, we remove barriers by pre-qualifying your business through industry-standard soft credit pulls. This protects your credit score while we identify the most aggressive lending partners for your specific profile. Whether you require SBA Loans, Credit Lines, or Equipment Financing, our team manages the complex origination process to reduce your time to funding. We act as the bridge between your current state and your future goals.

Our Tailored Funding Process

Our approach is methodical and designed to respect your time. We move quickly from a broad overview of your capabilities to specific categories of assistance.

Step 1: The Strategic Financial Check-Up. We analyze your cash flow, revenue patterns, and growth goals to identify the right capital product before you ever submit a formal application.

Step 2: Expert packaging. We translate your financials into "lender's language." We specialize in the updated $10 million SBA limits and specialized solutions like Purchase Order Financing and Factoring.

Step 3: Direct connection. We link you to a curated network of national lending partners who are actively deploying capital in the current 6.75% Prime Rate environment.

Start Your Consultation Today

Waiting for a traditional bank to issue a rejection can cost you weeks of vital growth. In 2026, proactive planning is the only way to navigate shifting interest rates and disclosure laws. When weighing direct business lenders vs brokers, remember that having a solution-focused ally in your corner simplifies the path to progress. We provide the steady, reliable hand you need to unlock your business's potential. Book an online consultation today to explore your tailored capital solutions and secure the Working Capital your business deserves.

Accelerate Your Growth with a Strategic Capital Strategy

The 2026 lending market moves quickly. Deciding between direct business lenders vs brokers shouldn't be a source of stress. It's a strategic choice that depends on your current credit profile and your specific growth goals. Whether you prioritize a singular bank relationship or require the broad market access of a dedicated guide, the goal remains the same: securing capital that fuels progress. You've learned that while direct paths offer simplicity, the broker model provides the competitive pressure necessary to optimize your capital stack.

Allen Capital Funding removes the guesswork from this process. We provide expert guidance for strategic business growth through our national lending network access. Our team specializes in tailored SBA and working capital solutions designed to meet the unique needs of your industry. By conducting a proactive financial check-up, we ensure you're positioned for the best possible terms before you ever submit an application. We act as your proactive ally, removing barriers and simplifying the path to your next milestone.

Don't let the complexity of modern finance slow your momentum. Book Your Strategic Funding Consultation with Allen Capital Funding today to explore your options. You have the vision for your business; we have the tools and connections to help you fund it.

Frequently Asked Questions

Do business loan brokers charge upfront fees?

Reputable business loan brokers generally do not charge upfront fees for their services. They typically earn a commission or success fee from the lender once your loan is closed and funded. You should be cautious of any intermediary requesting payment before you have received a formal offer or secured your capital. This model ensures the broker is motivated to find the best possible outcome for your business.

Is it always cheaper to go directly to a bank for a business loan?

Going directly to a bank is not always the most cost-effective path. While you might avoid an indirect referral fee, you miss out on the competitive bidding environment a broker creates among multiple funders. Brokers often negotiate lower interest rates or more flexible terms that offset any baked-in costs. In the 2026 market, the choice between direct business lenders vs brokers should focus on the total cost of capital over the life of the loan rather than just the initial fee.

Can a broker help if I have been rejected by a direct lender?

Yes, brokers specialize in finding alternative solutions when a traditional bank or direct lender issues a rejection. Denials are often based on rigid internal criteria or specific industry "hard stops" rather than your company's actual potential. A broker analyzes your cash flow and assets to match you with non-bank funders who have a higher appetite for your specific profile or industry risk. This proactive approach turns a "no" into a strategic path forward.

How does working with a broker affect my credit score?

Working with a professional broker often protects your credit score during the shopping phase. In 2026, it is the industry standard for brokers to use a soft credit pull for pre-qualification. This allow you to explore multiple funding options without the damage caused by several hard inquiries from different direct lenders. A hard pull typically only occurs once you select a specific lender and move toward final approval and closing.

What is the typical commission for a business loan broker in 2026?

Commissions for business loan brokers are typically paid by the lender rather than the borrower. The specific amount depends on the product type and the loan's total value; however, state-level disclosure laws in 2026 now require many providers to be transparent about total dollar costs. Working with an ally who clarifies these terms ensures you understand the full financial impact of your funding choice without hidden surprises.

Will a direct lender offer me the same products as a broker?

No, a direct lender is limited to the specific products they fund from their own balance sheet. A broker acts as a single point of entry to a diverse range of capital sources. While a bank might only offer a standard term loan, a broker can connect you with Credit Lines, Equipment Financing, and Factoring simultaneously. This allows you to build a more flexible capital strategy that isn't dependent on one institution's rigid product list.

How long does it take to get funded through a broker vs. a direct lender?

The time to capital depends heavily on whether you choose direct business lenders vs brokers. Traditional direct lenders like banks often take 2 to 8 weeks to finalize commercial loans due to legacy underwriting processes. Conversely, working with a broker to access online lenders or private debt funds can result in funding within 1 to 5 business days. Brokers accelerate the process by ensuring your application is complete and correctly packaged before any lender sees it.

Is SBA lending better handled by a bank or a specialist broker?

Specialist brokers are often better equipped to handle the complexities of SBA lending, especially with the 2026 increase in loan limits to $10 million. They understand the rigorous federal documentation requirements and can identify which SBA-approved lenders are currently the most responsive. This guidance reduces the risk of technical denials and ensures your application moves through the processing queue as efficiently as possible. Having an expert guide simplifies what is often the most difficult path to capital.

Comments