Business Line of Credit: The Strategic Guide to Flexible Capital in 2026

- anthonyarallen

- 12 minutes ago

- 12 min read

What if your biggest business constraint isn't your annual revenue, but simply your timing? You've likely felt the sting of missing a bulk inventory discount or delaying a critical hire because your cash is locked in outstanding invoices. Relying on high-interest credit cards often feels like a temporary fix that creates a long-term burden. This is where a business line of credit serves as a vital tool for your financial toolkit. It's not just a safety net; it's a strategic bridge that connects your current state to your future goals.

We understand that managing uneven cash flow requires more than just luck; it requires a reliable partner and the right financial structure. With the prime rate sitting at 6.75% as of July 2026, choosing the right capital structure is more important than ever. This guide will help you master the mechanics of revolving capital so you can access on-demand funds whenever opportunities arise. You'll learn how to pay interest only on what you use while building a robust credit history for your company. We'll break down the latest lending standards and show you how to leverage flexible capital to fuel sustainable, accelerated growth.

Table of Contents

What is a Business Line of Credit? Defining Your Strategic Safety Net

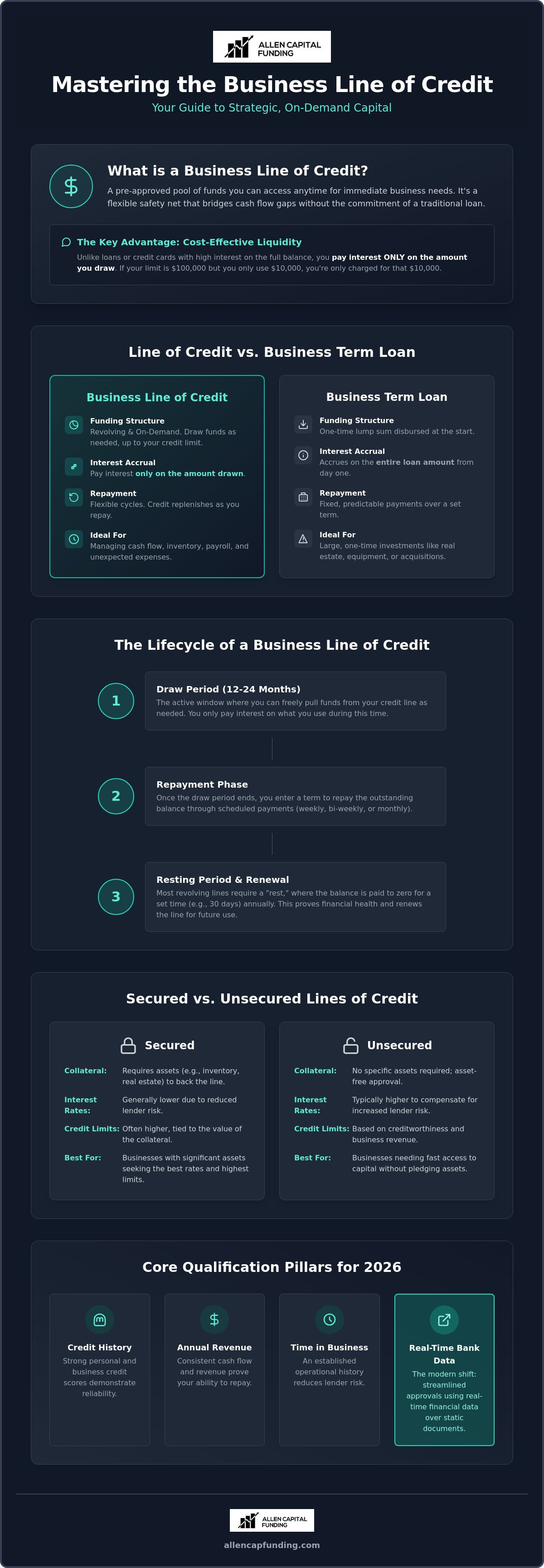

A business line of credit functions as a dynamic liquidity tool for the modern entrepreneur. It provides a pre-approved pool of funds that you can access at any time to meet immediate operational needs. Unlike other financing models, you aren't forced to take the full amount at once. You draw what you need, use it for a specific goal, and then repay it. This flexibility makes it a cornerstone of a healthy capital stack. While you might use SBA loans for major expansions or equipment financing for specific machinery, a line of credit handles the daily friction of business. To understand the broader financial context, it helps to ask: What is a line of credit? At its core, it is a revolving agreement that resets as you pay down your balance.

Think of it as a high-capacity resource for managing short-term cash flow gaps. Many owners compare it to a corporate credit card, but there is a distinct advantage. Lines of credit generally offer significantly lower interest rates than traditional credit cards. Most importantly, you only pay interest on the specific balance you've drawn, not the total limit available to you. If you have a $100,000 limit but only use $10,000 to cover an inventory purchase, you're only billed for that $10,000. This makes it an incredibly cost-effective way to maintain short-term liquidity without the burden of heavy interest on unused capital.

The Core Difference: Line of Credit vs. Business Term Loan

The primary distinction lies in how you receive and repay the funds. A business term loan provides a lump-sum disbursement. The moment the money hits your account, interest begins to accrue on the entire balance. This is ideal for one-time, fixed-cost investments like purchasing real estate. In contrast, a business line of credit offers on-demand draws. You control the timing and the amount. While term loans have fixed repayment schedules that can last years, lines of credit use flexible revolving cycles. You choose a line when you need a safety net for ongoing needs, such as seasonal inventory spikes or managing accounts receivable delays.

Revolving vs. Non-Revolving Lines

Most small businesses utilize a revolving structure. This means your available credit replenishes automatically as you pay back the principal. If you draw $20,000 and pay it back next month, that $20,000 becomes available for use again immediately. Non-revolving lines are less common and typically serve specific, one-off projects like construction phases. Once you spend the funds in a non-revolving line, the account closes. For daily operations, the revolving model is superior because it provides a permanent bridge between your current expenses and your future revenue.

How a Business Credit Line Works: Mechanics and Repayment

Maximizing the utility of a business line of credit requires a clear understanding of its operational lifecycle. Most credit facilities start with a defined draw period. This is the window of time, often spanning 12 to 24 months, where you're free to pull funds as needs arise. During this phase, you only pay interest on the capital you've actually deployed. Once the draw period concludes, you typically enter a repayment phase. You can't access new capital during this time, but you'll continue making scheduled payments until the balance reaches zero.

Repayment structures vary significantly depending on the lender and the specific product. You'll likely encounter weekly, bi-weekly, or monthly payment schedules. Selecting the right frequency is a strategic decision. If your business sees daily cash inflows, weekly payments might help you stay ahead of interest costs. If your revenue is more cyclical, monthly payments offer more breathing room. Following SBA guidance on business lines of credit can help you determine which structure aligns best with your cash flow projections. With the prime rate at 6.75% as of July 2026, understanding how these payments affect your bottom line is critical.

Lenders also look for signs of financial health through a "resting period." This policy requires you to pay the line down to a zero balance for a set duration, such as 30 consecutive days, at least once a year. It proves you aren't using the credit line as a permanent crutch for basic survival. It also resets your available credit, ensuring you're prepared for the next major opportunity. You can explore tailored funding solutions to find a facility that offers the flexibility your specific industry requires.

Common Fees to Watch For

Transparency is key when evaluating the total cost of capital. Origination fees are common and are typically charged as a percentage of your total credit limit. You should also check for draw fees, which apply every time you move money from the line to your operating account. Maintenance fees are recurring costs to keep the account open, while inactivity fees may apply if you don't use the line for six months or longer. Always calculate the total cost rather than just looking at the interest rate.

The Impact on Your Business Credit Score

A business line of credit is a powerful tool for building a professional credit profile. Lenders report your activity to agencies like Experian and Dun & Bradstreet. Consistent, on-time repayments demonstrate reliability to future creditors. However, you must manage your utilization ratio carefully. Keeping your balance below 30% of your total limit is a standard best practice. High utilization can lower your score, even if you never miss a payment. Strategic, small draws followed by prompt repayments keep your profile active and healthy.

Secured vs. Unsecured Business Lines: Navigating Risk and Collateral

Choosing the right structure for a business line of credit requires balancing immediate access against the long-term cost of capital. Lenders generally categorize these facilities into two groups: secured and unsecured. Unsecured lines are the hallmark of modern fintech lenders, offering rapid approval and funding without requiring specific collateral. While this speed is advantageous, it comes with a trade-off. Unsecured lines typically carry higher interest rates, often ranging from 10% to 16% APR for top-tier borrowers. Because the lender takes on more risk, they almost always require a Personal Guarantee (PG), making the business owner personally liable if the company defaults.

Secured lines are typically the domain of traditional banks and credit unions. These facilities are backed by tangible assets, which lowers the lender's risk and results in more favorable pricing. Rates for secured lines often fall between 8% and 14% APR. When you secure a line, the lender will likely file a UCC-1 financing statement. This creates a blanket lien on your business assets, ensuring the lender has a legal claim to your inventory, equipment, or accounts receivable in the event of non-payment. Understanding these legal filings is a critical part of choosing between a loan and a line of credit for your specific growth phase.

Asset-Based Lines of Credit

For businesses with significant balance sheet strength, asset-based lending offers a powerful way to scale. You can leverage your accounts receivable to increase your borrowing base, essentially turning unpaid invoices into immediate working capital. Retailers and manufacturers often use inventory-backed lines to prepare for peak seasons. Allen Capital Funding specializes in matching asset-rich businesses with these secured structures, ensuring you receive the maximum limit possible based on the true value of your collateral.

Which Option Fits Your Risk Appetite?

Startups and service-based companies often begin with unsecured lines because they lack the heavy equipment or real estate needed for collateral. As your company matures and acquires more assets, moving toward a secured business line of credit can significantly reduce your interest expenses. Before committing to any collateral, we recommend a comprehensive Financial Check-Up. This helps you evaluate the cost of capital against the risk of asset loss. A strategic guide can help you determine if the lower rate of a secured line justifies the administrative requirements and lien filings that come with it.

Qualification Strategy: Securing Approval in 2026

Securing a business line of credit in 2026 requires a shift in how you present your company's health. While historical data remains relevant, modern lenders have moved toward dynamic underwriting. They now prioritize real-time bank data over static tax returns that might be eighteen months old. By linking your accounting software or bank feeds directly to a lender's portal, you provide a transparent, live view of your cash flow. This shift allows for faster decisions and often results in higher credit limits for businesses with strong, consistent daily balances.

Preparing your financial profile for a large capital draw involves more than just cleaning up your books. You need to demonstrate that your business can handle the debt service even during seasonal dips. Lenders look for a healthy "debt service coverage ratio," typically wanting to see that your operating income is at least 1.25 times your total debt obligations. If your initial application faces a denial, don't view it as a dead end. Common reasons for rejection include recent credit inquiries or insufficient time in business. In these cases, you can pivot to alternative solutions like factoring or working capital loans to build the necessary track record for a future line of credit.

Minimum Requirements for 2026

Revenue Benchmarks: Most lenders now view $100,000 in annual gross revenue as the baseline floor. For unsecured products, this requirement often climbs to $250,000.

Credit Score Nuances: A personal FICO score of 600 is often the minimum, but top-tier rates usually require a 680 or higher. Lenders also increasingly use the FICO SBSS score, which blends your personal history with business data.

Time in Business: While some fintechs accept six months of history, the "golden zone" remains 12 to 24 months. This duration proves your business model has survived multiple quarterly cycles.

The Application Process: From Submission to Funding

The speed of your funding depends heavily on your choice of lender. Fintech platforms often provide same-day approval by using automated algorithms to scan your EIN, tax IDs, and recent bank statements. Traditional banks offer lower rates but require a deeper manual review that can take several weeks. Working with a dedicated guide can streamline this journey. A broker helps by submitting your profile to multiple compatible partners simultaneously, ensuring you don't waste time on lenders whose criteria you don't meet. If you want to accelerate your search for the right capital, contact Allen Capital Funding to explore our national network of lending partners today.

Strategic Funding with Allen Capital Funding: Your Dedicated Guide

Securing a business line of credit is often the first step in building a resilient capital stack. At Allen Capital Funding, we act as your proactive ally, ensuring this liquidity tool works in harmony with your broader financial goals. A line of credit provides the short-term agility you need, but it shouldn't exist in a vacuum. We help you integrate revolving capital with long-term solutions like SBA Loans for expansion or Equipment Financing for essential machinery. This holistic approach removes barriers to progress and ensures your business isn't over-leveraged on a single type of debt.

Our brokerage advantage gives you access to a national network of lending partners that single banks simply can't match. We don't believe in one-size-fits-all products. Instead, we focus on expert origination to accelerate your success. Our team understands the nuances of 2026 lending standards, allowing us to pivot quickly between different funding structures as market conditions change. This speed to capital ensures you can seize opportunities before they disappear. We act as a bridge between your current state and your future goals, providing the steady hand you need in a complex market.

Why Work with a Loan Specialist?

Managing complex financial terms is a full-time job. Working with our specialists allows you to focus on running your business while we handle the technical details. One of the biggest risks in modern finance is the "hard pull" trap. Applying blindly to multiple lenders can damage your credit score before you even receive an offer. We protect your profile by targeting the right lenders first. As your capital needs evolve, we stay by your side, adjusting your business line of credit strategy to support your next phase of growth.

Next Steps: Booking Your Consultation

Preparation is the key to securing the best terms. We recommend starting with a proactive Financial Check-Up to identify any gaps in your current profile. During your first strategy session, we'll review your revenue patterns, credit health, and specific goals. We'll then map out a clear path to the capital you need, whether that's a new credit line or a more complex funding bundle. Book your tailored funding consultation today.

Take Command of Your Capital Strategy

A business line of credit is more than a safety net for slow months. It's a strategic tool that allows you to act with speed when inventory discounts appear or expansion opportunities arise. By mastering the mechanics of revolving capital and understanding the 2026 shift toward real-time financial data, you position your company for sustainable growth. Whether you choose the lower rates of a secured line or the rapid access of an unsecured facility, the right choice depends on your specific risk appetite and cash flow patterns.

Allen Capital Funding provides the expert loan origination you need to navigate these financial decisions. With our national reach and dedicated team, we specialize in tailoring capital solutions that bridge the gap between your current operations and your future goals. We focus on your accelerated success by simplifying the complexities of SBA products and credit lines. Ready to stabilize your cash flow and fuel your next big move? Secure your business line of credit with expert guidance at Allen Capital Funding. Your business's potential is limitless when you have the right partner by your side.

Frequently Asked Questions

Is a business line of credit better than a business credit card?

A line of credit is often superior for large cash withdrawals and managing payroll, whereas credit cards are better for small daily purchases with rewards. Credit lines typically offer interest rates between 8% and 18% APR, which is significantly lower than the 20% to 30% APR common on business credit cards. Additionally, drawing cash from a card often triggers high transaction fees that you don't face with a credit line.

How much can I qualify for with a business line of credit?

Qualification limits vary based on your revenue and assets. Unsecured lines typically range from $10,000 to $500,000. If you provide collateral through a secured line, limits can reach $5 million or more. Most lenders cap your credit limit at 10% to 20% of your annual gross revenue. For example, a business earning $1 million annually might qualify for a $100,000 to $200,000 business line of credit.

Can I get a business line of credit with bad credit?

You can still secure funding with a personal credit score as low as 600, though your options will be more limited. Lenders may require a larger revenue history or specific collateral to offset the risk. In these cases, you might start with a smaller limit and higher interest rate. As you demonstrate a consistent repayment history, you can often negotiate for better terms or a limit increase as your profile strengthens.

What is the typical interest rate for a business line of credit in 2026?

Interest rates in 2026 are heavily influenced by the 6.75% prime rate. Traditional bank lines currently range from 8% to 14% APR for secured facilities. Online and fintech lenders offer faster access but higher rates, typically between 12% and 22% APR. Your specific rate depends on your FICO SBSS score, annual revenue, and whether you choose a secured or unsecured structure to back the facility.

Do I need to provide collateral for a small business line of credit?

Collateral isn't always mandatory. Many fintech lenders offer unsecured lines that rely on your cash flow and credit history instead of physical assets. However, these often require a personal guarantee. If you want the lowest possible interest rates or a significantly higher limit, providing collateral like accounts receivable or equipment can make your application much stronger and more competitive in the eyes of a lender.

How long does it take to get approved and funded?

Approval speeds depend on the lender's technology. Fintech platforms can often provide an approval decision in minutes and fund your account within 24 to 48 hours. Traditional banks follow a more manual process that includes a deep dive into your financial history, which can take two to four weeks. We help you choose the right path based on how quickly you need to deploy capital for your operations.

Can a new business get a line of credit?

Most lenders require at least 12 to 24 months of operational history to qualify. However, some specialized fintech lenders will consider startups with only six months of history if they show strong, consistent monthly revenue. If your business is brand new, you might need to provide a personal guarantee or collateral to secure a business line of credit while you build your company's credit profile from the ground up.

What happens if I do not use my business line of credit?

You won't accrue interest charges if your balance stays at zero. This makes it an ideal tool for emergency preparedness. You should check your agreement for inactivity or annual maintenance fees, as some lenders charge a small fee to keep the line open even if it isn't used. Keeping the line open without a balance can actually help your credit score by improving your available credit ratio over time.

Comments